Articles

Articles

Smart Ways to Reduce Your Debt

by Mitali Dutta Elearnmarkets - Financial Market EducationDebt has penetrated every level of our society from the individual to the government. Relying on credit and building credit card debt has become unavoidable for some and a way of life for many especially younger generations. It usually starts with irresponsible use of credit cards and grows worse as unanticipated circumstances like unemployment, medical emergencies or sudden changes in a family situation come into the picture.

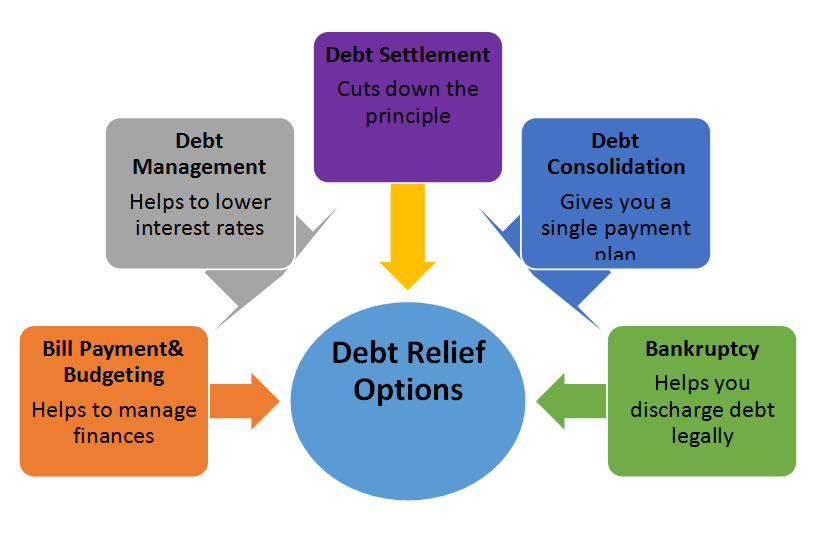

There are various Debt relief options available to lighten your financial stress and improve your financial health.

Debt settlement and debt consolidation are two common debt relief financial solutions, which may help people struggling with more debt than they can repay. Both options can reduce and eliminate your debt. But each will have different consequences on your credit score and future financial options. Before choosing either option, educate yourself on the pros and cons of each.

Debt Settlement

Debt settlement, also called debt negotiation, is a process where settlements are negotiated with your unsecured creditors, where they agree to forgive a part of your debt, which leads to saving you around 40% to 60% of what you owe. Results can vary widely. Debt settlement can be done by your own, or you can work with a reputable debt settlement company.

After a settlement is reached, you pay the reduced, agreed-upon amount in a lump-sum payment. In some cases, you can pay this settled balance in payments, over a structured period of time.

Pros

· Significantly reduce your total debt.

· Instant financial relief in your monthly budget. And the rest of your debt payments are much more manageable.

· Faster than a debt payment plan.

· The impact on credit profiles often is less than that of a bankruptcy filing.

Cons

· Continuous call from creditors during the negotiation process or creditors can pursue legal action.

· Negative impact on your credit rating due to not making minimum payments.

· You must pay a fee to the debt negotiation company for its services.

· You might have to pay income tax on the forgiven debt amount.

Debt Consolidation

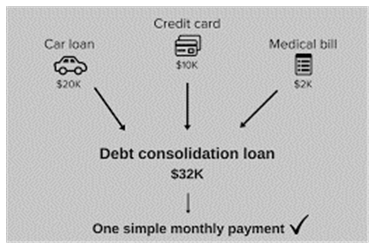

Debt consolidation is the process of accumulating numerous debts into one loan, hopefully at reduced interest rate with one lower monthly payment.

A debt consolidation loan is a personal loan that allows you to consolidate your credit card debt, line of credit, car loan, and similar debt, into a single loan. This way, you only have one monthly payment instead of multiple.

Some people undertake this process on their own, whether through balance-transfer credit card offers, a home equity loan (using the proceeds to repay other debts) or a personal loan. Others opt to work with debt consolidation services, who help consolidate debt for a fee on top of the interest on the loans.

Apart from debt management, with consolidation, a company negotiates lower interest rates with your creditors. Leading you to save money on interest. You make one monthly payment to the debt consolidation company, and they handle paying all your accounts.

Pros

· Predictable monthly payment and predictable interest rate.

· Debt consolidation loans often have a fixed amortization period, which provides the ability to pay debt down in a specific time period.

· Interest rates on debt consolidation loans typically are much lower than interest rates on credit cards; and in the case of using a home equity loan to consolidate debt, the interest may be tax-deductible.

Cons

· This option might not be available to people with poor credit or no income;

· The monthly payment may be higher than credit card payments, even with a lower interest rate (given a shorter payback period).

· Loans secured against a home or vehicle put those assets at risk if you fail to make timely payments on the loan.

· You will not reduce the overall total of your debt.

Which is the Best for Your Situation?

Debt Settlement is a viable option for people who are struggling to make minimum payments, and who are willing to dedicate themselves to a process lasting two to four years. People who are not in a hardship, and who have the ability and self-discipline to pay down their debt and fight charging up balances on other credit cards, might find debt consolidation useful.

Sponsor Ads

Created on Sep 21st 2017 00:24. Viewed 527 times.