The Lexington Group Tokyo New York Asia Financial Services: Stretch IRA strategy

The “stretch

IRA” is not a type of IRA; it’s a wealth-transfer strategy. If you

don’t anticipate needing all of your IRA assets to provide income in

retirement, you may be able to stretch your IRA assets to benefit your spouse,

children and grandchildren.

The stretch

strategy begins with your UBS IRA. It is important to work with your Financial

Advisor to properly designate your beneficiaries and ensure they understand how

the stretch IRA strategy works.

The benefits of stretching your IRA

– Throughout

the life of the IRA, you and your beneficiaries will enjoy the benefits of

tax-deferred growth on the assets.

– You and your

beneficiaries have the opportunity to receive an income stream over the longest

allowable period until the IRA assets are eventually exhausted.

– If

beneficiary designations are properly set up, your IRA passes directly to your

heirs, giving them access to that money without potential time delays and fees.

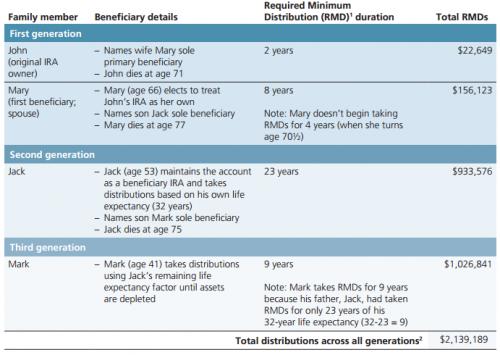

How it works

Once you reach

age 70½, you are required to withdraw annual required minimum distributions

(RMDs) from your traditional IRAs. The amount of your RMDs is based on two

factors: your IRA account value and your life expectancy. Since both factors

change every year, so will the amount you are required to distribute. The

IRA begins to be “stretched” when it passes to your primary beneficiary upon

your death. In most cases, a younger spouse can roll your IRA over to their own

IRA to “reset” the RMD formula to reflect his or her longer life expectancy—thus

“stretching” out the RMDs over more years. The same concept works as the second

generation inherits your spouse’s IRA—the next beneficiary may also “reset” the

RMD amounts to his or her own life expectancy, and “stretch” the period of

distributions. The third generation cannot “reset” the RMDs to their own life

expectancy, but they will benefit from the years of tax-deferred growth of the

assets and will receive the distributions until the account is depleted.

Stretching a Roth IRA

The stretch IRA strategy also works with a Roth IRA. Since RMDs are not required from a Roth IRA during your lifetime, you pass your entire Roth IRA to your heirs who can generally take tax-free distributions from the account over their life expectancy.Contact us to discuss beneficiary planning and how you and your family can benefit from the stretch IRA strategy.

Post Your Ad Here

Comments