How to Start Retirement Planning in Your 20s, 30s, and 40s

In India, retirement planning often takes a back seat to immediate financial goals like buying a house or funding children’s education. However, the earlier you start, the easier it becomes to build a sufficient retirement corpus. Whether you are in your 20s, 30s, or 40s, the right strategy at the right time can help you secure a financially independent future. Let’s break it down decade-wise.

Starting

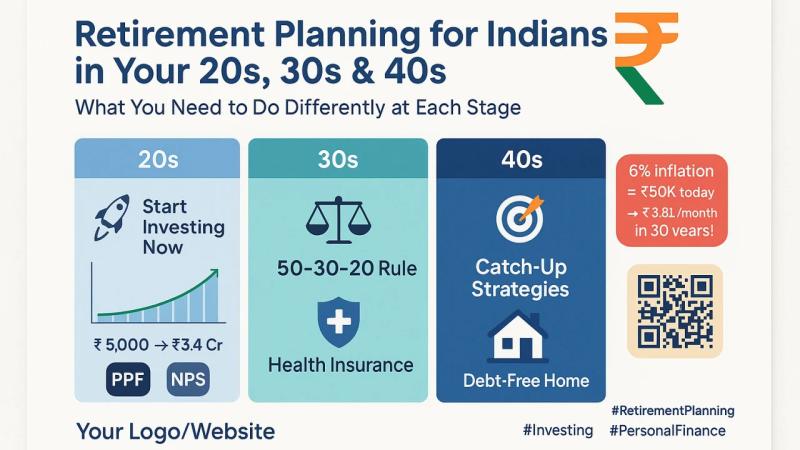

in Your 20s: The Power of Early Action

Your 20s are the golden years for

retirement planning. Time is your biggest asset because it allows the power of

compounding to work in your favor. Starting early means you can invest smaller

amounts and still build a substantial corpus over time.

Key Steps:

- Begin with SIPs: Systematic Investment Plans

(SIPs) in equity mutual funds are an excellent way to start. With a long

horizon, equities can outpace inflation and grow wealth.

- Open an NPS Account: The National Pension System

(NPS) is a government-backed scheme offering tax benefits and a

disciplined retirement saving approach.

- Set Financial Goals: Even if retirement feels

decades away, setting a target amount based on expected expenses helps you

stay focused.

- Invest Aggressively: At this stage, your risk

appetite is high. Allocate more towards equities (around 80%) and lesser

to debt instruments.

Tip: Start with even ₹500 a month if

that’s all you can afford. The habit is more important than the amount

initially.

Planning

in Your 30s: Balancing Growth and Responsibilities

Your 30s typically come with

increased financial responsibilities — marriage, children, home loans. However,

it’s also the decade when your income stabilizes and grows, giving you more

investing capacity.

Key Steps:

- Increase Contributions: As your salary increases,

step up your SIP amounts by at least 10% annually.

- Diversify Investments: Apart from equities, include

Public Provident Fund (PPF), EPF (Employees’ Provident Fund), and debt

mutual funds to create a balanced portfolio.

- Purchase Adequate Insurance: Secure your family’s future

with term insurance and health insurance. Retirement savings should not be

derailed by medical emergencies.

- Evaluate Retirement Corpus: Reassess your retirement goal

considering inflation, lifestyle upgrades, and family needs.

Tip: A thumb rule is to invest at least

20-25% of your monthly income towards retirement savings at this stage.

Catching

Up in Your 40s: Strategic and Focused Moves

If you’ve delayed retirement

planning until your 40s, don't panic. You still have two decades left but need

a more aggressive and disciplined approach.

Key Steps:

- Maximize Savings: Save a higher percentage (up

to 35-40%) of your income towards retirement.

- Invest Smartly: Create a mix of moderately

aggressive investments — a 60:40 split between equity and debt works well.

- Use Tax-Advantaged Instruments: Maximize benefits under

Section 80C through investments in ELSS, PPF, and NPS.

- Consider Annuities and

Retirement Plans:

Start looking into retirement-specific products like pension plans or

annuities to secure regular income post-retirement.

- Minimize Debt: Aim to become debt-free

before you retire. Pay off home loans and personal loans to reduce

financial burdens later.

Tip: It's critical to review and adjust

your investment portfolio every year to stay on track.

Final

Thoughts

No matter your age, the best time to

start retirement planning is now. Starting in your 20s gives you a massive

advantage, but even a late start in your 40s can be salvaged with focused

efforts. In the Indian context, where joint families are transitioning to

nuclear ones and healthcare costs are rising, financial independence after

retirement is crucial.

Adopt a disciplined approach, stay consistent with investments, and adapt your strategies as your life circumstances change. Your future self will thank you for the financial freedom you secured today.

Would you also like me to create a

short summary version (around 150 words) for social media sharing?

Post Your Ad Here

Comments